- Healthcare 150

- Posts

- From Pandemic Necessity to Market Opportunity: The Business of Telemedicine

From Pandemic Necessity to Market Opportunity: The Business of Telemedicine

The healthcare industry is undergoing a digital transformation, and at the forefront is telemedicine, reshaping how patients access care and how providers deliver it.

The healthcare industry is undergoing a digital transformation, and at the forefront is telemedicine, reshaping how patients access care and how providers deliver it. What was once a niche offering has now become a critical component of modern healthcare, with online doctor consultations surging from 40.8 million users in 2018 to a projected 130.4 million by 2028. The shift toward virtual healthcare solutions is not just about convenience; it’s a response to evolving patient expectations, cost efficiencies, and technological advancements.

For investors and healthcare executives, the opportunity in telehealth is substantial, spanning digital infrastructure, AI-driven diagnostics, and hybrid care models. With projected revenues climbing from $23.8 billion in 2023 to $35.8 billion by 2028, the market is maturing into a stable, high-growth sector. This report unpacks the key trends driving telehealth adoption, the financial outlook, and the investment landscape—providing a roadmap for those looking to capitalize on the next wave of healthcare innovation.

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.

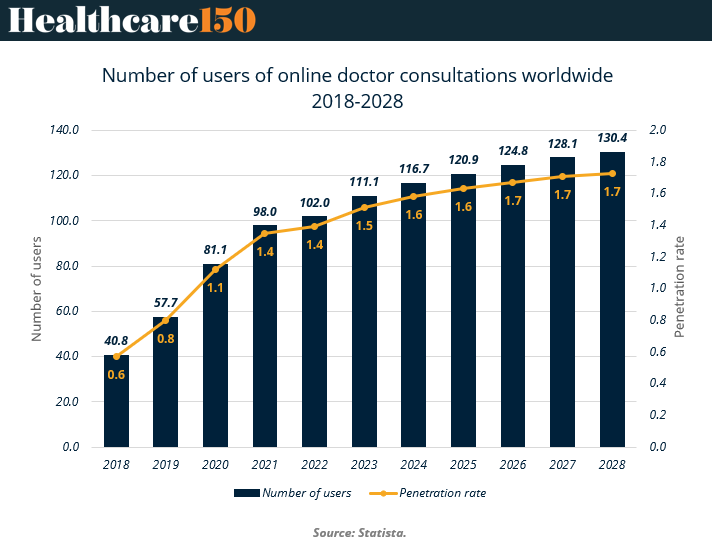

Online doctor consultations

The adoption of online doctor consultations has grown rapidly over the past decade, transforming healthcare delivery worldwide. From 40.8 million users in 2018 to a projected 130.4 million by 2028, this market reflects a shift toward digital-first solutions that prioritize convenience, accessibility, and efficiency. This growth has been particularly accelerated by the pandemic, which normalized telemedicine as a viable alternative to in-person consultations.

The penetration rate of online consultations, relative to total doctor visits, is projected to climb steadily, from just 0.6% in 2018 to 1.7% by 2028, signaling a growing consumer preference for digital healthcare. While penetration rates may seem modest, the consistent upward trajectory highlights the untapped potential of telemedicine in addressing global healthcare challenges, especially in underserved and remote areas.

For healthcare investors and executives, the opportunity lies in capturing this sustained growth by expanding telehealth infrastructure, integrating with traditional care, and innovating patient experiences. With the telemedicine market maturing globally, the data emphasizes the need for scalable, user-friendly platforms that meet the demands of a diverse and growing user base.

Key takeaways from chart

Rapid User Growth:

The number of online doctor consultation users is projected to grow from 40.8 million in 2018 to 130.4 million in 2028, more than tripling in a decade.

Key milestones include surpassing 100 million users in 2022, driven by the pandemic and increasing telehealth acceptance.

Steady Rise in Penetration:

The penetration rate is projected to rise from 0.6% of doctor consultations in 2018 to 1.7% by 2028, reflecting growing adoption across demographics and geographies.

While annual growth in penetration rates will stabilize at 1.7% from 2025 onward, this steady trajectory highlights the normalization of telemedicine globally.

Opportunities for Investment:

Emerging markets and underserved regions offer significant potential for scaling telehealth platforms.

Growth drivers include consumer demand for convenience, cost efficiency, and the expansion of high-speed internet access globally.

Mature markets present opportunities to integrate telehealth with in-person care for hybrid healthcare models.

Market Resilience:

The slight plateau in growth post-pandemic reflects the market’s transition from early adoption to mainstream utilization, underscoring its permanence in healthcare delivery.

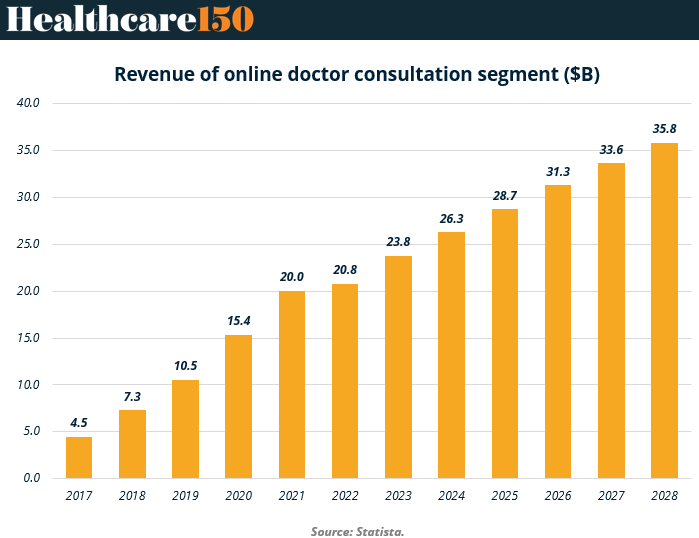

The financial state

The online doctor consultation market has witnessed remarkable revenue growth, surging from $4.5 billion in 2017 to $23.8 billion in 2023. This trajectory underscores the sector's ability to address increasing global demand for telehealth solutions. As the pandemic accelerated adoption, revenues more than doubled from $10.5 billion in 2019 to $20 billion in 2021, establishing telemedicine as a cornerstone of modern healthcare delivery.

From 2024 onward, the market is projected to maintain its robust growth, reaching $35.8 billion by 2028. This forecast reflects the sector’s maturity, driven by expanded digital infrastructure, patient preference for convenience, and integration into mainstream healthcare systems. The stable annual growth from 2024 highlights the lasting impact of telemedicine adoption beyond its pandemic-driven surge.

For healthcare investors and executives, this data signals a prime opportunity to capitalize on scalable digital health platforms, innovative care delivery models, and emerging markets. The focus now shifts to optimizing user experiences and integrating telemedicine into hybrid care systems to sustain this revenue momentum.

Key takeaways from chart

Historical Revenue Growth:

Revenue rose from $4.5 billion in 2017 to $23.8 billion in 2023, a fivefold increase in six years.

The steepest growth occurred between 2019 and 2021, highlighting the pandemic’s role in accelerating adoption.

Forecasted Expansion (2024–2028):

Revenue is projected to climb steadily, reaching $35.8 billion by 2028, reflecting continued market confidence and adoption.

Annual revenue growth stabilizes post-2024, suggesting the transition to a mature, predictable growth phase.

Key Growth Drivers:

Consumer demand: Convenience and access in underserved areas.

Technological advancements: Enhanced digital platforms and AI integration for improved patient experiences.

Policy support: Expanding reimbursement policies and government backing for telehealth adoption.

Investment Implications:

Opportunities in platform scalability and emerging markets where telehealth remains underdeveloped.

Potential for vertical integration with physical healthcare providers to create hybrid care solutions.

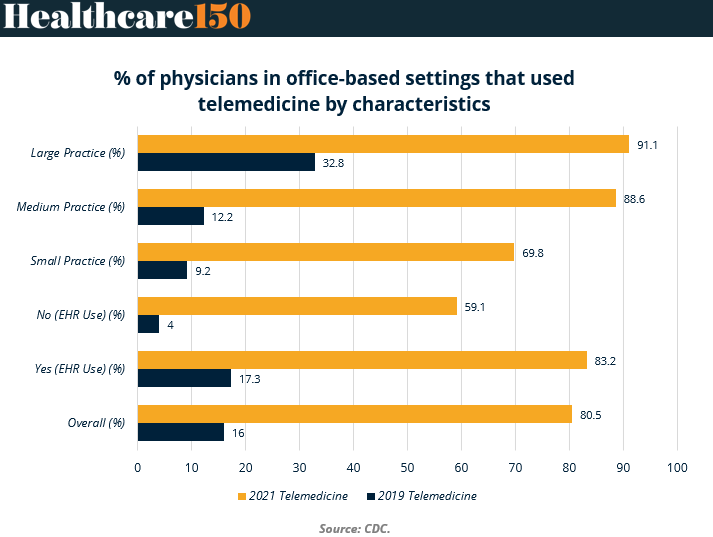

The Pandemic’s Transformational Impact on Telemedicine Adoption

The COVID-19 pandemic dramatically accelerated the adoption of telemedicine in office-based physician settings, as reflected in the jump from 16% overall usage in 2019 to 80.5% in 2021. This surge underscores how the pandemic served as a catalyst for integrating digital healthcare solutions into routine practice. Physicians across practice sizes and technology use cases embraced telemedicine to maintain care delivery amid lockdowns and patient safety concerns.

Large practices saw the most significant adoption rates, with telemedicine usage soaring from 32.8% in 2019 to 91.1% in 2021, reflecting their ability to deploy infrastructure quickly. Even smaller practices, traditionally slower to adopt digital tools, experienced a substantial increase, with adoption rising from 9.2% to 69.8% over the same period.

Electronic Health Record (EHR) systems also played a crucial role in scaling telemedicine, with physicians using EHRs reaching 83.2% adoption in 2021, compared to just 17.3% in 2019.

This rapid digital transformation highlights the resilience and adaptability of healthcare systems in crisis. For executives and investors, the data illustrates the permanence of telemedicine as a mainstream care delivery model, presenting opportunities to further enhance integration, improve patient experiences, and invest in technology infrastructure.

Key Takeaways from chart

Overall Surge:

Telemedicine usage across all physicians increased from 16% in 2019 to 80.5% in 2021, driven by the pandemic’s demand for remote care solutions.

Adoption by Practice Size:

Large Practices: Usage jumped from 32.8% to 91.1%, showcasing their capacity to scale technology quickly.

Medium Practices: Adoption rose significantly, from 12.2% in 2019 to 88.6% in 2021, nearly matching large practice levels.

Small Practices: Telemedicine use grew from 9.2% to 69.8%, reflecting a broader shift toward digital tools, even in resource-constrained settings.

Impact of EHR Use:

Physicians using EHRs saw adoption rise from 17.3% in 2019 to 83.2% in 2021, emphasizing the role of integrated systems in telehealth scalability.

Practices without EHRs lagged, with adoption increasing from 4% to 59.1%, highlighting a gap in technological readiness.

Implications for the Future:

The widespread adoption of telemedicine, even in smaller and less digitally equipped practices, reflects the pandemic’s role in reshaping care delivery.

Opportunities exist to close the technology gap for non-EHR users and enhance telehealth infrastructure for smaller practices, particularly in underserved regions.

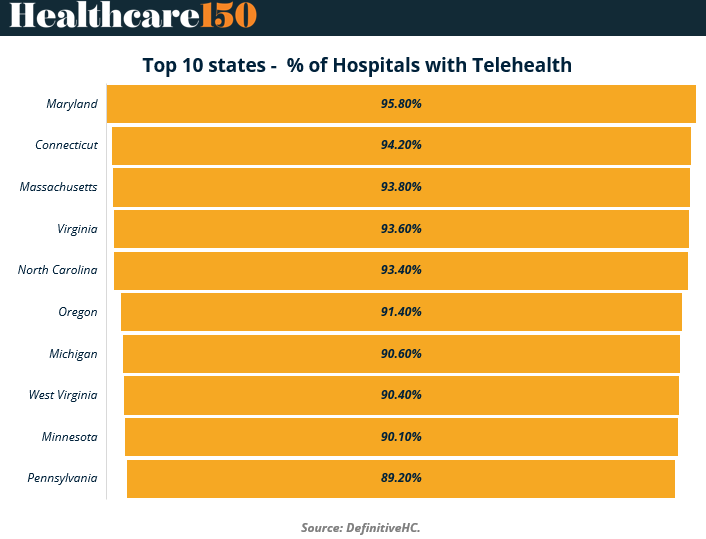

Top States Leading Telehealth Adoption in Hospitals

Telehealth adoption in hospitals has reached significant penetration levels across the United States, with the top 10 states boasting adoption rates exceeding 89%. Leading the pack is Maryland, where 95.8% of hospitals offer telehealth services, closely followed by Connecticut (94.2%) and Massachusetts (93.8%). These states highlight a growing commitment to integrating digital tools into healthcare delivery, making telemedicine a standard practice.

What sets these states apart is their strong healthcare infrastructure, robust policy support, and high levels of digital readiness. For example, many of these states have implemented telehealth-friendly legislation, ensuring reimbursement parity for virtual visits and funding for technology adoption. Furthermore, the concentration of academic medical centers and healthcare systems in states like Massachusetts and Michigan contributes to early and widespread adoption of telehealth services.

This high adoption demonstrates the ability of hospitals in these regions to meet rising patient demand for convenience and access, particularly in the wake of the COVID-19 pandemic. For stakeholders, these top-performing states serve as a model for scaling telehealth services through effective policymaking, funding initiatives, and leveraging regional healthcare ecosystems.

Key Takeaways from chart

Top 3 States Leading Adoption:

Maryland (95.8%): Strong healthcare networks and state-level incentives for digital health expansion.

Connecticut (94.2%): Proactive policies ensuring telehealth parity and expanded broadband access.

Massachusetts (93.8%): Presence of advanced academic medical institutions driving innovation and adoption.

High Adoption in Southeastern States:

Virginia (93.6%) and North Carolina (93.4%) showcase how proactive reimbursement policies and robust hospital networks have supported adoption.

Notable Presence in the Midwest:

Michigan (90.6%) and Minnesota (90.1%) reflect efforts to bridge care gaps in rural areas through telemedicine expansion.

Policy and Infrastructure as Key Enablers:

Telehealth-friendly policies, including reimbursement parity and technology grants, have spurred adoption in these states.

Investments in high-speed internet infrastructure, particularly in rural areas, ensure that hospitals can deliver quality virtual care.

Lessons for Other States:

States with lagging adoption rates can look to these leaders for best practices, including integrating telehealth into existing healthcare systems and incentivizing its use among providers and patients alike.

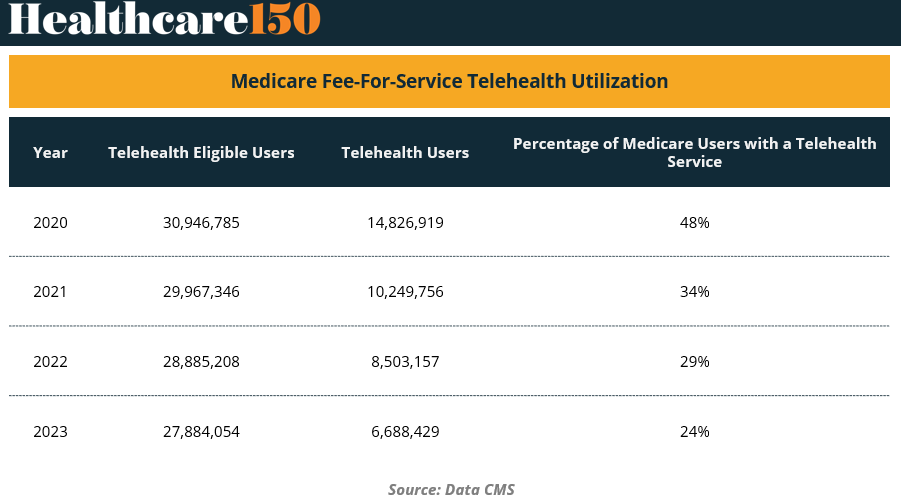

Medicare covered telehealth

The use of telehealth among Medicare Part B Fee-for-Service beneficiaries has seen a sharp decline since its peak in 2020, reflecting the sector's transition from pandemic-driven highs to more sustainable utilization levels. In 2020, 48% of eligible users accessed telehealth services, a record high driven by the need for remote care during the COVID-19 pandemic. However, as healthcare systems reopened for in-person services, this number dropped to 24% by 2023.

The data also highlights a consistent reduction in both the total number of telehealth-eligible users and actual users over the years. Eligible users declined from 30.9 million in 2020 to 27.8 million in 2023, while telehealth users fell from 14.8 million to 6.6 million during the same period. This suggests a normalization of healthcare delivery post-pandemic, where telehealth complements rather than replaces traditional care.

For healthcare executives and investors, these shifts present opportunities to refine telehealth offerings. The focus should now shift to improving user engagement, integrating hybrid care models, and targeting populations that benefit most from virtual healthcare, such as rural communities and patients with mobility challenges.

Key Takeaways from chart

Pandemic Peak (2020):

48% of eligible users accessed telehealth services, totaling 14.8 million users, reflecting the rapid adaptation to remote care during COVID-19.

Post-Pandemic Decline:

By 2023, utilization fell to 24% of eligible users, with only 6.6 million users, as in-person care resumed.

The decline underscores telehealth's shift from a pandemic necessity to an adjunct in care delivery.

Declining Eligibility Pool:

The number of telehealth-eligible users decreased from 30.9 million (2020) to 27.8 million (2023), likely due to changes in CMS policies or demographic shifts.

Opportunities for Stakeholders:

Target underutilized groups to boost engagement, particularly in rural or underserved areas.

Focus on chronic care management and behavioral health, which remain strong candidates for telehealth.

Strengthen hybrid care models that integrate virtual and in-person visits, creating a seamless patient experience.

Sources & References

Definitive HC. Hospitals Telehealth Adoption. https://www.definitivehc.com/resources/healthcare-insights/hospital-telehealth-adoption-by-state

Data CMS. Telehealth Snapshot. https://data.cms.gov/sites/default/files/2024-12/f5b35fbf-002a-425d-924d-f99aa362a63f/Medicare%20Telehealth%20Trends%20Snapshot%2020241127_508.pdf

CDC. NHSR Data. https://www.cdc.gov/nchs/data/nhsr/nhsr210.pdf

Statista. Telemedicine. Penetration rate of online doctor consultations worldwide 2018-2029

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.