- Healthcare 150

- Posts

- Charting the Future: Why EHR is the Backbone of Modern Medicine

Charting the Future: Why EHR is the Backbone of Modern Medicine

The Electronic Health Records (EHR) market stands at the forefront of healthcare's digital revolution, offering transformative solutions that improve clinical workflows, enhance patient care, and address complex regulatory requirements.

Table of Contents

The Electronic Health Records (EHR) market stands at the forefront of healthcare's digital revolution, offering transformative solutions that improve clinical workflows, enhance patient care, and address complex regulatory requirements. As healthcare providers increasingly adopt advanced technologies like artificial intelligence and interoperability tools, the EHR sector has evolved into a critical enabler of innovation and operational efficiency.

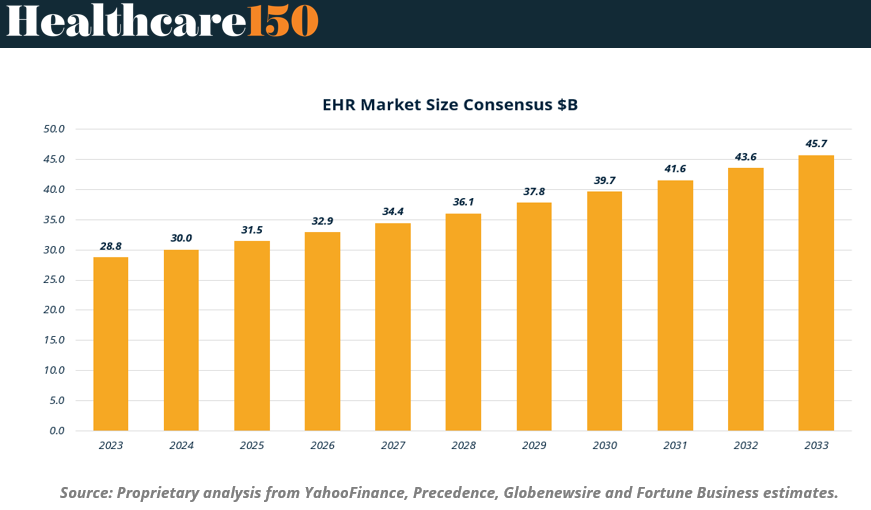

With global market size projections surging from $28.8 billion in 2023 to $45.7 billion by 2033, this growth presents a compelling opportunity for investors to capitalize on the demand for cutting-edge healthcare IT solutions. This report explores the dynamic landscape of the EHR market, adoption trends, and the investment potential within this rapidly expanding sector.

EHR Market Size

The global Electronic Health Records (EHR) market represents a dynamic and rapidly expanding sector, one that is becoming increasingly critical to the future of healthcare. With digital transformation accelerating across industries, the healthcare space is leveraging EHR solutions to streamline operations, enhance patient outcomes, and improve decision-making for care providers. These systems have moved beyond simple data repositories and are now integral tools for clinical workflows, compliance, and patient engagement. For investors, the EHR market is a compelling opportunity that combines high growth potential with the increasing demand for innovation in healthcare delivery.

As shown in the chart below, the EHR market is on a consistent growth trajectory, with consensus projections showing the market size expanding from $28.8 billion in 2023 to an impressive $45.7 billion by 2033. This growth is fueled by the ongoing adoption of advanced technologies like artificial intelligence, cloud computing, and interoperability solutions. Regulatory mandates and value-based care initiatives are further driving adoption, creating a fertile environment for continued investment and innovation. For decision-makers in the healthcare investment space, understanding this growth story and its underlying drivers is critical for identifying and capitalizing on opportunities in this evolving market.

Takeaways from chart

Steady Growth Trajectory: The market is expected to grow from $28.8 billion in 2023 to $45.7 billion by 2033, reflecting a robust compound annual growth rate (CAGR).

Key Drivers of Expansion: Growth is driven by technological advancements, including AI-powered EHR solutions, increased focus on interoperability, and regulatory pressures such as the CMS interoperability rules.

Shift Towards Value-Based Care: The shift from fee-for-service models to value-based care is encouraging healthcare providers to adopt EHR systems to meet data management and reporting requirements.

Regional Opportunities: The North American market remains dominant, but emerging markets in Asia-Pacific are expected to see accelerated adoption due to expanding healthcare infrastructure.

Private Equity Interest: With consolidation trends in healthcare, private equity firms are actively investing in EHR providers to capitalize on growing demand and scalable recurring revenue models.

Barriers to Watch: Despite strong growth, challenges such as high implementation costs, data security concerns, and provider resistance to change could impact adoption rates.

EHR Adoption

The adoption of Electronic Health Records (EHRs) has witnessed a dramatic transformation over the past decade, marking a pivotal shift in the healthcare landscape. What began as a slow uptake in the early 2000s has accelerated into near-universal adoption in hospitals and significant progress among office-based physicians. This widespread implementation underscores the growing reliance on digital tools to enhance healthcare delivery, improve patient outcomes, and meet evolving regulatory requirements.

As the chart below illustrates, the adoption of certified EHRs by hospitals surged from just 9% in 2008 to an impressive 96% by 2014, maintaining that level through 2021. Similarly, office-based physicians have shown substantial progress, with adoption rates increasing from 17% in 2008 to 78% in 2021. This remarkable growth reflects the healthcare sector's commitment to leveraging technology to streamline operations and support data-driven care. For investors and stakeholders, understanding these adoption trends provides critical insights into the market dynamics and opportunities within this evolving sector.

Key takeaways from chart

Rapid Hospital Adoption: Adoption of certified EHRs in hospitals grew exponentially, reaching 97% by 2014 and maintaining 96% adoption through 2021, reflecting widespread standardization across the sector.

Steady Progress Among Physicians: Office-based physicians have made significant strides, with EHR adoption increasing from 17% in 2008 to 78% by 2021, highlighting a broader shift toward digitization in smaller practices.

Key Milestones: By 2011, adoption among hospitals jumped to 28%—a critical turning point—while physicians reached 34%, driven by federal incentives under the HITECH Act.

Saturation Levels Achieved: The plateau in hospital adoption at 96% indicates the market has reached saturation, shifting focus to optimization, upgrades, and new feature adoption.

Investment Opportunities: With near-universal adoption, opportunities lie in enhancing interoperability, data analytics, and AI-driven solutions that add value to existing systems.

Challenges for Office-based Physicians: Despite progress, smaller practices face cost and complexity barriers, presenting an opportunity for scalable, user-friendly EHR solutions tailored to their needs.

Deals & funding

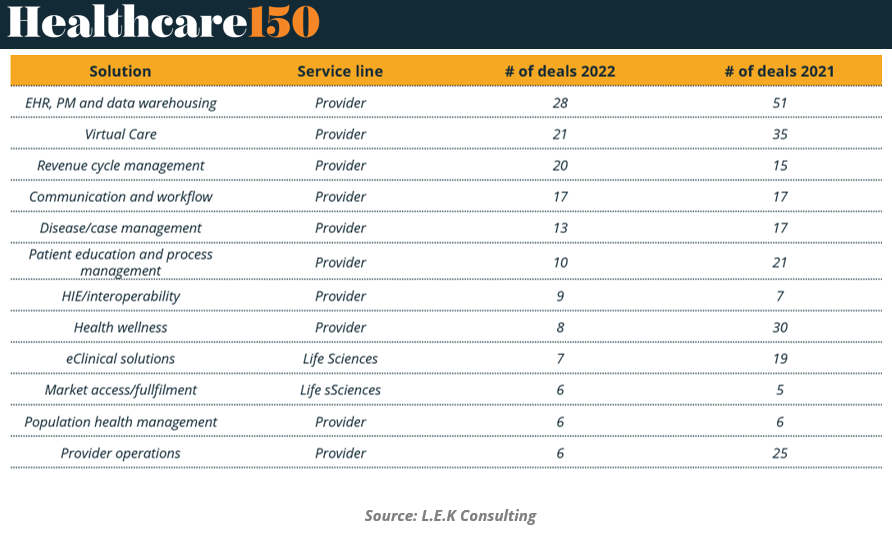

The healthcare technology market is evolving at an unprecedented pace, and the private equity space is closely monitoring the segments that hold the greatest potential for growth and consolidation. The chart presented provides a snapshot of the deal activity in various healthcare solutions from 2021 to 2022, offering a clear picture of the shifting priorities within the industry. With the electronic health records (EHR), practice management (PM), and data warehousing segment dominating the field, and virtual care gaining momentum, this data underscores where capital deployment is trending. Moreover, the decline in specific categories such as provider operations suggests an adjustment in focus, perhaps influenced by evolving demands for innovation and efficiency.

For private equity executives and advisors, these trends provide a strategic roadmap for evaluating market opportunities. Whether it's scaling existing portfolio investments or identifying new segments ripe for disruption, understanding these shifts can help ensure alignment with market needs and maximize returns. The data not only highlights where the deals are happening but also signals the long-term strategic priorities reshaping the healthcare landscape.

Key takeaways from chart

EHR, PM, and Data Warehousing

Maintained the highest number of deals in both years (28 in 2022, 51 in 2021), reflecting continued dominance.

The significant drop from 51 to 28 deals suggests market saturation or consolidation in this segment.

Virtual Care

Marked growth with 21 deals in 2022, though slightly down from 35 in 2021. Highlights ongoing interest in remote patient management and telehealth solutions.

Investors should consider expanding in niche telehealth platforms or services catering to underserved populations.

Revenue Cycle Management

Increased deal count from 15 in 2021 to 20 in 2022, showcasing heightened demand for efficiency in healthcare billing and collections.

Strong potential for investments in automation and AI-driven solutions in this area.

Communication and Workflow

Steady deal activity with 17 deals each year, indicating consistent demand. Suggests a stable market with room for differentiation via user-friendly and integrated platforms.

Disease/Case Management

Declined slightly from 17 deals in 2021 to 13 in 2022. Indicates potential challenges in scaling or integrating such solutions but still presents value for chronic disease management innovations.

Patient Education and Process Management

Sharp decline from 21 deals in 2021 to 10 in 2022, signaling waning interest or market saturation. Investors may want to explore personalized education tools leveraging AI and mobile applications.

HIE/Interoperability

Modest growth from 7 deals in 2021 to 9 in 2022, highlighting gradual progress in data-sharing infrastructure. High potential for future growth, given regulatory and industry pushes for seamless data exchange.

Health Wellness

Decline from 30 deals in 2021 to 8 in 2022, suggesting reduced PE interest.

Opportunities may remain in targeting niche wellness solutions linked to mental health or corporate wellness programs.

eClinical Solutions

Significant drop from 19 deals in 2021 to 7 in 2022, reflecting diminished focus. Could still hold potential for investments targeting life sciences innovations and clinical trial optimizations.

Market Access/Fulfillment

Growth from 5 deals in 2021 to 6 in 2022, indicating a slow but steady interest in ensuring therapies and solutions reach target markets effectively.

A burgeoning area for portfolio diversification in life sciences.

Population Health Management

Stable with 6 deals in both years, showing continued yet limited interest. Investors could focus on integrated platforms combining analytics and patient outreach for better outcomes.

Provider Operations

Notable decline from 25 deals in 2021 to 6 in 2022, suggesting a pivot away from operational platforms. Signals potential for disruption with innovations in provider workflow optimization.

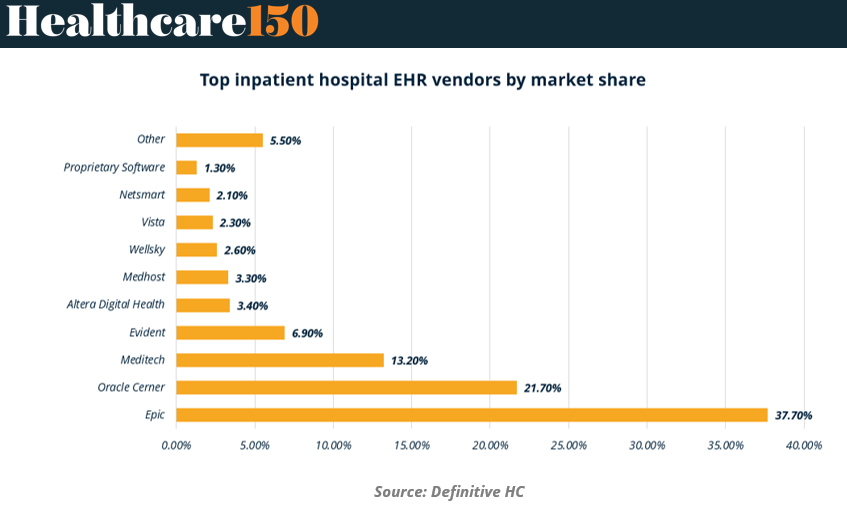

The inpatient hospital EHR (Electronic Health Record) market is dominated by a few major players, creating a highly concentrated competitive landscape. As seen in the chart, Epic leads the market with a commanding 37.7% share, followed by Oracle Cerner with 21.7%, and Meditech at 13.2%. Together, these three vendors account for over 70% of the market, reflecting their deep penetration in the hospital systems space. Smaller players like Evident, Altera Digital Health, and Medhost make up a smaller but still relevant portion of the market, while niche and proprietary solutions demonstrate the ongoing demand for tailored solutions.

For investors and healthcare executives, this data illustrates a dual challenge and opportunity: navigating a market dominated by established giants while identifying areas for disruption or differentiation. The dominance of Epic and Oracle Cerner highlights their scalability and ability to meet complex system needs, while the presence of smaller competitors points to the potential for niche innovation, particularly in underserved segments or smaller hospital systems. This environment presents significant opportunities for consolidation, partnerships, or investments in next-generation EHR platforms that prioritize interoperability and usability.

Key takeaways from chart

Epic (37.7% Market Share)

Maintains a dominant lead in the inpatient hospital EHR market, representing over a third of the market.

Renowned for its scalability and broad functionality, making it a preferred choice for large hospital systems.

Offers significant opportunities for complementary solutions or partnerships for those targeting the Epic ecosystem.

Oracle Cerner (21.7% Market Share)

A strong second player in the market, with robust adoption across mid-to-large-sized hospitals.

Recently boosted by Oracle's acquisition, likely driving more investment in cloud and AI capabilities.

Meditech (13.2% Market Share)

Positioned as a significant player, particularly in smaller and mid-sized hospital systems.

Potential for growth by targeting cost-conscious hospitals and improving interoperability features.

Evident (6.9% Market Share)

Represents a moderate market share, catering to smaller or rural hospitals that may prioritize affordability.

Could be a target for M&A activity as larger players seek to expand into these segments.

Smaller Vendors (Altera Digital Health, Medhost, Wellsky, Netsmart, etc.)

Each occupies 3.4% or less of the market, reflecting niche solutions or regional dominance.

Opportunities for these players include offering highly specialized solutions or targeting underserved market segments.

Proprietary Software and "Other" (6.8% Combined Market Share)

Indicates ongoing interest in custom-built or unique solutions tailored to specific hospital needs.

Reflects the importance of flexibility and innovation, especially in cases where standard platforms fall short.

Concentration of Market Power

The top three players collectively control over 70% of the market, underscoring limited room for new entrants.

Potential disruption may come from next-gen platforms focusing on seamless data exchange, patient engagement, and advanced analytics.

Conclusion

As the EHR market continues its trajectory of robust growth, driven by technological innovation, regulatory mandates, and the global shift toward value-based care, the opportunities for investment and innovation remain significant.

Dominated by a handful of key players, the market also offers avenues for disruption in niche segments such as AI-driven analytics and interoperability solutions. Challenges like high implementation costs and data security concerns persist but underscore the need for scalable, user-friendly innovations. For investors and stakeholders, understanding the nuanced dynamics of this evolving market is crucial for identifying opportunities that align with the healthcare industry’s digital future.

With the EHR market poised for continued expansion, it is clear that the integration of technology into healthcare delivery is no longer optional, it is essential.

Sources & References

Yahoo finance. Global electronic health records Market. https://finance.yahoo.com/news/global-electronic-health-records-market-190000072.html

Precedence Research. Electronic health records Market Size. https://www.precedenceresearch.com/electronic-health-records-market

GlobenewsWire. Global electronic health records Market Size to reach $42B by 2033: https://www.globenewswire.com/news-release/2024/03/05/2840662/0/en/Electronic-Health-Records-EHRs-Market-Size-to-Reach-USD-41-87-Bn-by-2033.html

Fortune. Electronic health records Market. https://www.fortunebusinessinsights.com/electronic-health-records-ehr-market-102660

HealthitGov. National trends hospital and physician adoption EHR. https://www.healthit.gov/data/quickstats/national-trends-hospital-and-physician-adoption-electronic-health-records

LEK. HCIT deal landscape. https://www.lek.com/insights/hea/us/ei/hcit-deal-landscape-analysis-ma-activity

DefinitiveGC. Most common EHR systems. https://www.definitivehc.com/blog/most-common-inpatient-ehr-systems