- Healthcare 150

- Posts

- Biotech Boom: A Market on the Rise

Biotech Boom: A Market on the Rise

The biotechnology industry is at an inflection point, poised for unprecedented growth, innovation, and investment opportunities.

Table of Contents

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.

The biotechnology industry is at an inflection point, poised for unprecedented growth, innovation, and investment opportunities. With market projections skyrocketing from $1.51 trillion in 2023 to $4.91 trillion by 2033, biotech is reshaping healthcare, agriculture, and sustainability at a breakneck pace. From gene editing and mRNA breakthroughs to AI-driven drug discovery, cutting-edge advancements are pushing the boundaries of what’s possible—offering solutions to some of the world’s most pressing challenges.

Yet, investment trends tell a more nuanced story. After a record $48.3 billion in biotech dealmaking in 2021, investor enthusiasm has moderated, reflecting macroeconomic headwinds and shifting risk appetites. While funding dipped to $18.1 billion in 2023, the appetite for high-impact, scalable biotech ventures remains strong. The focus has shifted toward later-stage investments, strategic partnerships, and transformative technologies that can redefine industries.

This report breaks down market growth, investment trends, regional dynamics, and emerging opportunities in biotechnology. Whether you’re an investor, entrepreneur, or industry leader, understanding where the capital is flowing and which innovations are gaining traction is critical. The next decade of biotech will be shaped by game-changing breakthroughs, evolving funding landscapes, and global demand for cutting-edge solutions—and those who stay ahead of the curve will be best positioned to capitalize on the industry’s next big leap.

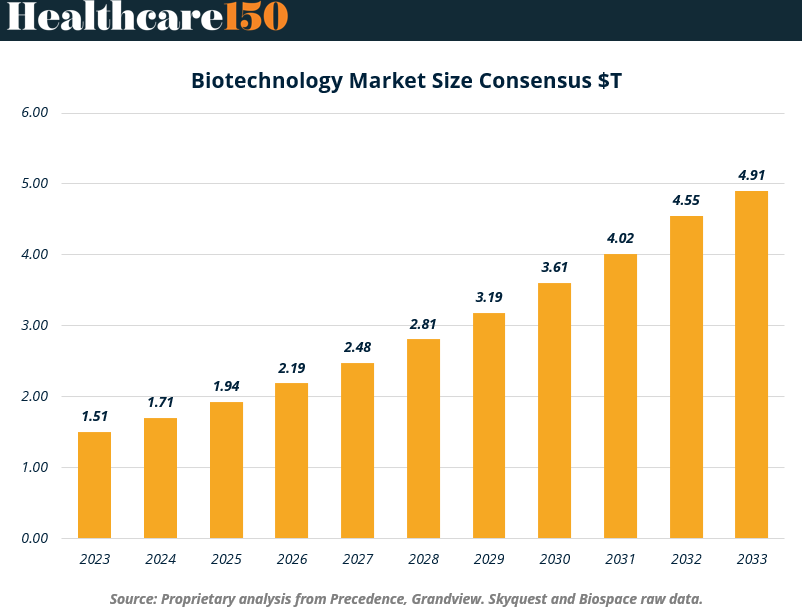

Biotechnology Market Size

The biotechnology market continues to demonstrate remarkable growth, driven by advancements in genetic engineering, personalized medicine, and biopharmaceutical innovation.

As a key driver of innovation in healthcare, agriculture, and industrial applications, biotechnology plays a pivotal role in addressing global challenges such as disease prevention, food security, and environmental sustainability. To provide a comprehensive understanding of the sector's potential, we have synthesized data from various reputable sources, culminating in a proprietary market size consensus.

Our analysis reveals a robust and sustained growth trajectory for the biotechnology market, with the consensus projecting an increase from $1.51 trillion in 2023 to $4.91 trillion by 2033. This represents a compound annual growth rate (CAGR) of approximately 12.2%, reflecting the sector's resilience and capacity for innovation. The following chart and analysis detail the anticipated growth and underlying drivers shaping this dynamic industry.

Key takeaways from chart

Market Growth Dynamics:

The biotechnology market is expected to grow from $1.51 trillion in 2023 to $4.91 trillion in 2033, more than tripling in value.

The CAGR of approximately 12.2% underscores the increasing global demand for biotech solutions.

Key Growth Years:

The market size shows accelerated growth between 2028 and 2031, with an annual increase of over $0.4 trillion in each of those years.

Notable milestones include surpassing the $2 trillion mark in 2026 and the $4 trillion mark in 2031.

Major Catalysts:

Advancements in drug discovery and development, particularly in biologics and gene therapies.

Expansion in agricultural biotechnology driven by the need for sustainable farming practices.

Rising global healthcare demands, especially in emerging markets, fueling innovation and market expansion.

Implications for Investors:

Significant opportunities exist in early-stage biotechnology ventures and breakthrough platforms.

The increasing emphasis on personalized medicine and genomics provides lucrative avenues for investment.

Emerging markets and global collaborations present additional opportunities for strategic partnerships.

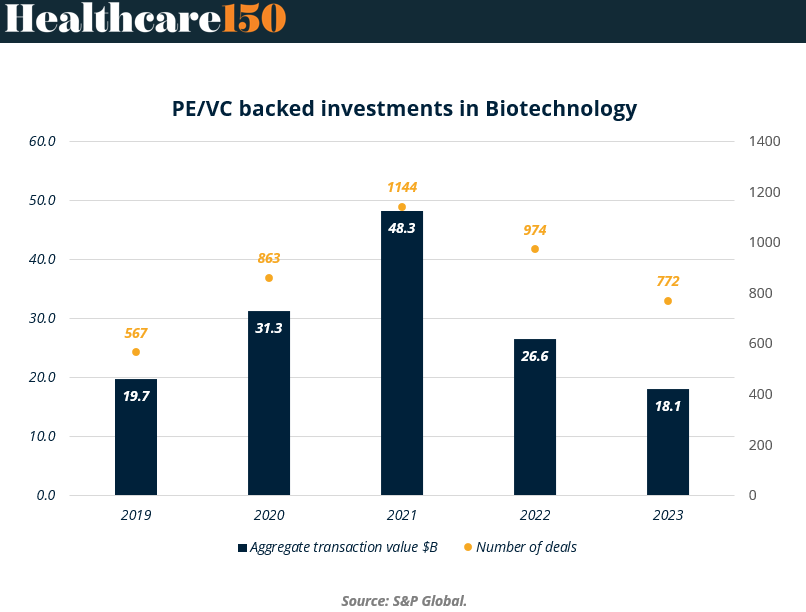

Investments / fundraising in Biotechnology

Private equity (PE) and venture capital (VC) have emerged as pivotal sources of funding for the biotechnology sector, reflecting investor confidence in the industry's transformative potential. These investments fuel critical innovation, enabling biotech companies to develop groundbreaking therapies, technologies, and solutions that address global challenges in healthcare and beyond. The trajectory of PE/VC-backed investments provides valuable insights into how capital has flowed into the industry over recent years and the evolving dynamics shaping the fundraising landscape.

From 2019 to 2023, the biotechnology sector experienced fluctuating levels of investment activity, with transaction values peaking in 2021 at $48.3 billion across 1,144 deals. This surge highlights a period of intense investor enthusiasm and deal-making, followed by a decline in activity amid macroeconomic uncertainties. As the sector recalibrates, the data underscores the resilience of biotech investments and the continued appetite for high-potential opportunities.

Key takeaways from chart

Investment Trends Over Time:

The aggregate transaction value rose significantly from $19.7 billion in 2019 to a peak of $48.3 billion in 2021, representing more than a twofold increase.

After the 2021 peak, investment activity declined, with transaction values falling to $26.6 billion in 2022 and $18.1 billion in 2023.

Deal Volume:

The number of deals also peaked in 2021, with 1,144 transactions, reflecting a period of heightened investor activity and biotech innovation.

Deal volume moderated in subsequent years, with 974 deals in 2022 and 772 in 2023, indicating a more cautious investment environment.

Key Drivers of Peak Activity (2021):

Increased interest in biotech solutions during the COVID-19 pandemic spurred record investments.

Breakthroughs in gene therapy, mRNA technology, and diagnostics attracted significant funding.

Post-2021 Decline:

Macroeconomic headwinds, including rising interest rates and global uncertainty, contributed to reduced investment levels in 2022 and 2023.

Investors have shifted focus to de-risking strategies, favoring later-stage ventures and proven technologies.

Outlook for Investors:

Despite recent declines, the sector remains a long-term growth opportunity, with unmet needs in healthcare driving demand for innovation.

Early-stage ventures, particularly in emerging areas like synthetic biology and precision medicine, offer promising opportunities for high returns.

A shift toward strategic collaborations and partnerships may define the future of biotech fundraising.

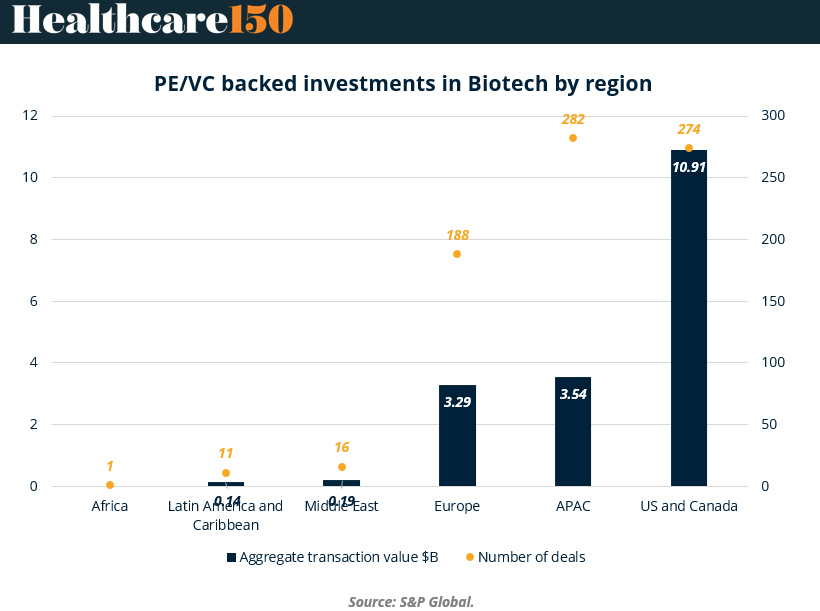

Regional Analysis

Private equity (PE) and venture capital (VC) investments in biotechnology vary significantly by region, reflecting diverse market dynamics, innovation ecosystems, and funding environments. The United States and Canada dominate the biotechnology investment landscape, benefiting from a mature ecosystem, robust research infrastructure, and established funding networks. Meanwhile, regions such as Europe and Asia-Pacific (APAC) are experiencing growing interest, driven by increasing innovation and favorable government policies.

Emerging markets such as Africa, Latin America, and the Middle East have yet to capture significant biotech funding, indicating potential opportunities for growth as these regions develop their biotechnology sectors. The geographic distribution of investment highlights both established powerhouses and untapped potential, providing a strategic perspective on where investors are currently focused and where future opportunities might arise.

Key takeaways from chart

Regional Highlights:

United States and Canada:

At $10.91 billion across 274 deals, this region leads global PE/VC investments in biotech.

Factors driving this dominance include a strong R&D ecosystem, world-class universities, and high investor confidence.

APAC:

The Asia-Pacific region attracted $3.54 billion across 282 deals, showcasing significant deal activity.

Rapid growth is fueled by government-backed initiatives and advancements in biopharma and diagnostics.

Europe:

Europe secured $3.29 billion across 188 deals, reflecting a thriving biotech innovation scene, particularly in countries like Germany, the UK, and Switzerland.

Emerging Markets:

Middle East:

With $0.19 billion across 16 deals, the Middle East is gradually building a presence, driven by increasing interest in healthcare innovation.

Latin America and Caribbean:

At $0.14 billion across 11 deals, this region shows modest activity but has potential for growth, particularly in agricultural biotechnology.

Africa:

With just $0.01 billion and 1 deal, Africa represents a nascent market with significant room for future development.

Key Trends:

The dominance of North America highlights the importance of developed ecosystems in attracting large-scale funding.

APAC and Europe are increasingly competitive, driven by their growing biotech capabilities and supportive regulatory frameworks.

Emerging regions remain underfunded, but advancements in infrastructure and policy could unlock future investment opportunities.

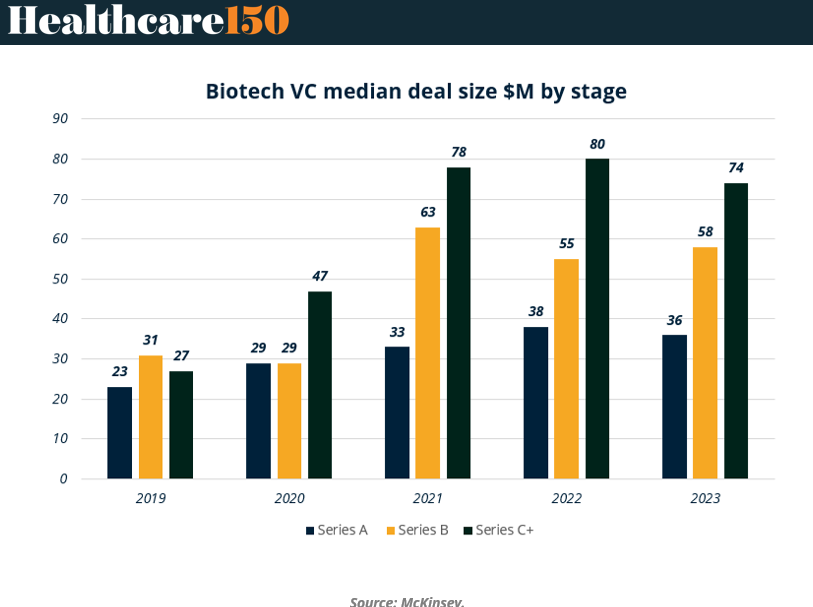

Biotech deals breakdown

The median deal size for venture capital (VC) investments in biotechnology has shown a clear upward trajectory over recent years, particularly in later funding stages such as Series C and beyond.

This trend reflects the increasing capital intensity of biotech ventures, as companies move closer to regulatory approval, product commercialization, or large-scale clinical trials. Larger deal sizes indicate greater investor confidence in scaling these ventures, driven by their potential for transformative breakthroughs and significant market impact.

From 2019 to 2023, the median deal size for all funding stages has risen, with Series C+ consistently commanding the highest funding levels. Series B investments have also seen substantial growth, highlighting the crucial role of mid-stage funding in advancing biotech innovations. Meanwhile, Series A deal sizes have grown more modestly, reflecting a focus on early-stage innovation but with slightly more conservative funding levels compared to later stages. This data underscores the growing importance of strategic funding allocation across different stages of the biotech lifecycle.

Key takeaways from chart

Overall Growth Trends:

Median deal sizes have grown across all stages from 2019 to 2023, emphasizing the increasing financial requirements of biotech companies.

Series C+ deals have shown the most substantial growth, peaking at $80M in 2022 and remaining high at $74M in 2023.

Series-Specific Insights:

Series A:

Starting at $23M in 2019, Series A median deal sizes grew modestly to $36M by 2023.

This reflects consistent interest in early-stage innovation, though funding levels are lower than later stages.

Series B:

Median deal sizes rose significantly, from $27M in 2019 to $58M in 2023.

The sharp increase highlights the pivotal role of Series B funding in scaling promising biotech ventures.

Series C+:

Series C+ deals commanded the largest funding, growing from $31M in 2019 to $80M in 2022, before settling slightly at $74M in 2023.

This stage consistently attracts the most capital, indicating investor focus on companies nearing market readiness.

Key Year of Growth:

The largest year-over-year increase occurred between 2020 and 2021, with Series C+ median deal sizes rising from $47M to $78M.

This jump coincided with heightened investment interest during the pandemic, driven by the demand for innovative biotech solutions.

Implications for Investors:

Later-stage investments offer opportunities to support companies closer to commercialization, often with lower risk compared to earlier stages.

Growth in Series B deal sizes suggests a strong mid-stage pipeline, signaling opportunities for scalable innovations.

Early-stage (Series A) funding remains critical for fostering next-generation biotech platforms, despite its smaller relative growth.

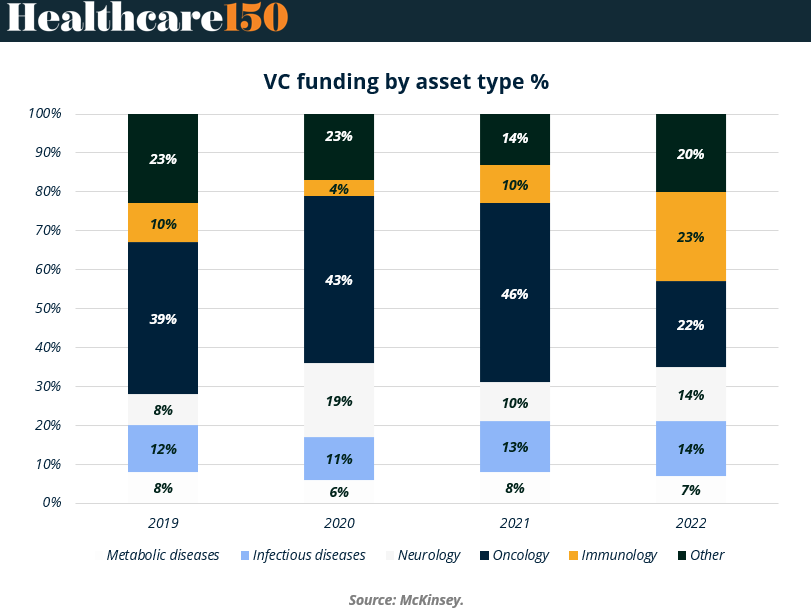

Biotech funding by type of assets

Venture capital (VC) funding in biotechnology has been distributed across various asset types, reflecting the diverse areas of innovation within the industry. Over the years, oncology has consistently captured the largest share of VC funding, showcasing its prominence as a focus for investment. However, shifts in funding distribution reveal evolving priorities among investors, with increased attention to infectious diseases, particularly during the COVID-19 pandemic, and growing interest in immunology and metabolic diseases in recent years.

From 2019 to 2022, the allocation of VC funding by asset type illustrates the dynamic nature of biotechnology investment. While oncology remains a dominant area, funding for infectious diseases surged in 2020 and maintained a notable presence in subsequent years. Similarly, neurology and immunology have gained steady support, indicating a broadening focus beyond traditional investment areas. This diversified funding pattern underscores the sector's potential to address a wide range of unmet medical needs.

Key takeaways from chart

Dominance of Oncology:

Oncology consistently received the largest share of funding, peaking at 46% in 2021 before declining to 22% in 2022.

This highlights oncology’s long-standing role as a primary driver of biotech innovation, though its share has recently contracted.

Rise of Infectious Diseases:

Funding for infectious diseases surged to 19% in 2020, likely driven by the COVID-19 pandemic, before stabilizing at 14% in 2021 and 2022.

This shift reflects investor interest in pandemic preparedness and infectious disease innovation.

Emergence of Immunology and Metabolic Diseases:

Immunology funding increased to 14% in 2022, reflecting growing interest in therapies targeting autoimmune diseases and immune-based treatments.

Metabolic diseases saw modest but consistent funding, ranging from 6% to 8%, underscoring their relevance in addressing chronic conditions.

Evolving "Other" Category:

The "Other" category represented 23% of funding in 2019, with its share decreasing to 14% in 2021 before rebounding to 20% in 2022.

This variation suggests fluctuating interest in niche or emerging therapeutic areas.

Shifts in Neurology:

Neurology funding remained steady, averaging around 10-13% over the years, emphasizing consistent interest in treatments for neurological disorders.

Implications for Investors:

Diversification across asset types reflects an adaptive approach to addressing both longstanding and emerging medical needs.

The resurgence of focus on infectious diseases and immunology presents new opportunities for investors in response to shifting global health priorities.

Oncology, while still critical, faces increased competition as investors explore a broader range of therapeutic areas.

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.

Sources & References

Precedence. Biotechnology market. https://www.precedenceresearch.com/biotechnology-market

Grandview Research. Industry Analysis: Biotechnology. https://www.grandviewresearch.com/industry-analysis/biotechnology-market

Skyquestt. Report: Biotechnology market. https://www.skyquestt.com/report/biotechnology-market#:~:text=Biotechnology%20Market%20size%20was%20valued,one%20of%20the%20globalized%20sectors.

Biospace. Biotechnology Market Size. https://www.biospace.com/biotechnology-market-size-to-reach-usd-5-68-trillion-by-2033

S&P Global. Private Equity Deal Value in Biotechnology. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/1/private-equity-deal-value-in-biotechnology-drops-by-32-in-2023-80108512#:~:text=Private%20equity%20and%20venture%20capital,number%20since%20at%20least%202019.

McKinsey. What Early stage investing reveals about biotech innovation. https://www.mckinsey.com/industries/life-sciences/our-insights/what-early-stage-investing-reveals-about-biotech-innovation